What is Driving BC Craft Beer Forward in 2015?

The 2014 Beer Me BC Craft Beer Survey is complete and this year more than 1500 respondents completed the survey with their opinion on the status of craft beer in British Columbia. With the amount of data collected and the comparative nature of the information this year’s results will be released in a number of steps focusing on different areas of the state of Craft Beer in BC. The first article is about the state of craft beer right now and the opinions of British Colombians on the matter.

From a statistical perspective this survey does not represent a random sampling but rather a gathering of perspective from those who have a vested interest in craft beer and have expressed interest in the industry by participating in the survey. Despite this non-random sampling technique the sample size is statistically significant to represent the province of British Columbia in the interests of those actively engaged in the consumption of Craft Beer.

Of the sample no questions listed below were considered mandatory except for the age. This was done to ensure that all participants are of legal age in the province of British Columbia. Because of this fact there are no respondents under the age of 19 and sums of submissions for each question will amount to less than the total of 1505 survey submissions.

Of respondents to the 2014 Beer Me BC Craft Beer Survey 34% responded as female while 66% of respondents were male. This number does not accurately represent the population of British Columbia but does illustrate the bias involved in surveying a craft beer-interested audience which is male dominated.

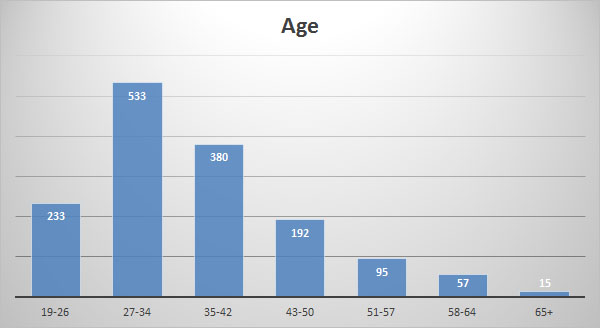

In the survey responses the mode (most prevalent) response is from the 27-34 age category. Similarly the Median (middle) response fit in the upper echelon of the 27-34 respondents insinuating (not statistically) that the median age is approximately 34 years.

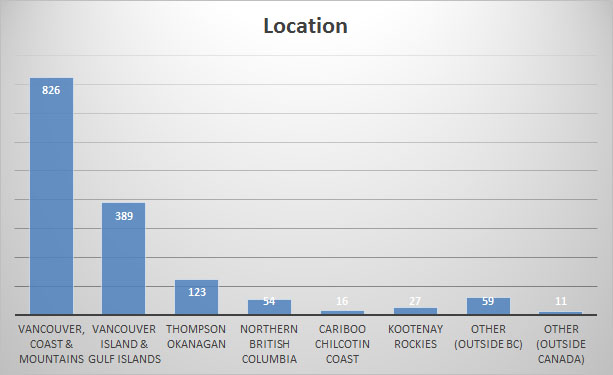

A total of 55% of all respondants were from the Vancouver Coast & Mountain Regions of British Columbia representing a bias towards the South West corner of the province. With 26% from Vancouver Island & Gulf Islands plus 8.2% from the Thompson Okanagan these numbers are large enough to be considered statistically relevant for these regions as well.

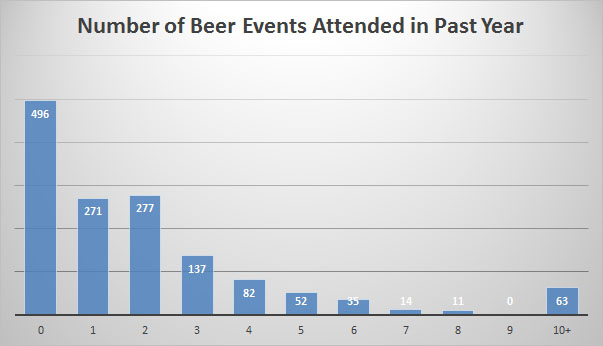

Beer events are something that have not always been well attended but from the responses of this survey we have the ability to extrapolate the data.The mean (average) number of events attended by survey respondants was 1.97*. At an average cost of $50 to attend an event this represents approximately $140,000 added to the BC economy.

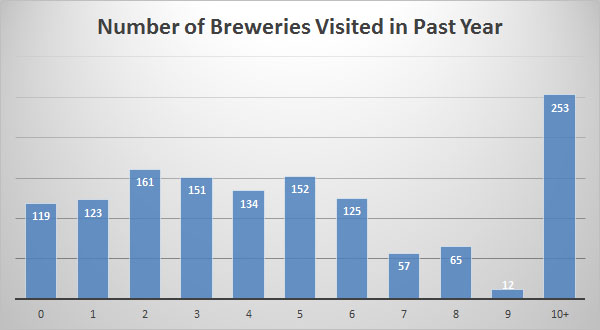

Even more impressive than the number of events attended is the number of breweries visited. At an average of 4.8 per respondent this is more than 6500 brewery visits in total. If each visit resulted in a $20 purchase this represents an additional $130,000 added to the BC economy.

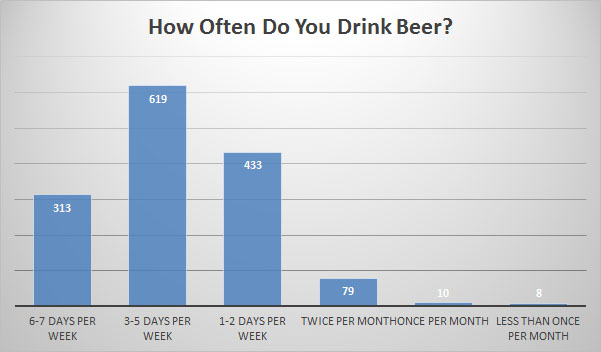

Consumption statistics are very interesting as well. From the results of this survey we know that 93.4% of respondents have at lease one beer per week. If we take the median of each frequency range and use 355ml as a standard serving size the extrapolate we can calculate that over 96,000 litres of beer was consumed in the past year. At an average of $3.00 per serving this equates to over $810,000 added to the BC economy.

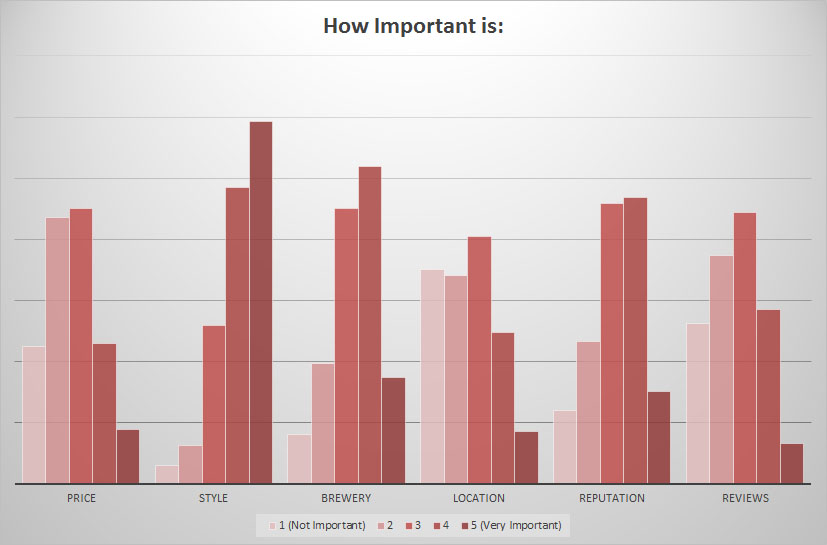

The decision making factors in purchase behaviour is very important and rather interesting. There is a great deal of information in the exhibit above and here is a breakdown of how these items line up.

- 4.08 Mean Importance – Beer Style

- 3.36 Mean Importance – Brewery

- 3.21 Mean Importance – Reputation

- 2.66 Mean Importance – Price

- 2.66 Mean Importance – Reviews

- 2.57 Mean Importance – Location

These numbers show that each aspect is of relative importance in the purchase decision process. Most important is style however and least important is the location of the brewery.

British Columbia residents have embraced craft beer. So much so that 62% of all respondents said that they are planning to visit a brewery more than 100km from their residence in the next 12 months.

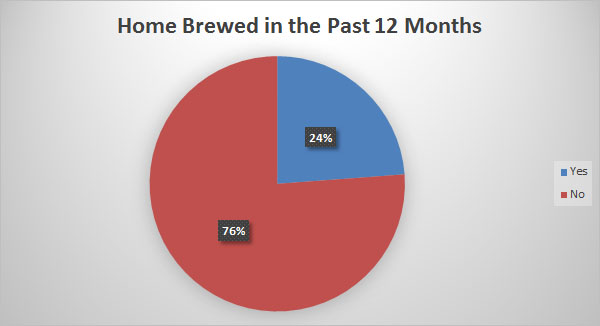

Home Brewing has exploded in British Columbia recently. While it is a small piece of the pie 24% of respondents said that they have brewed beer at home in the past 12 months.

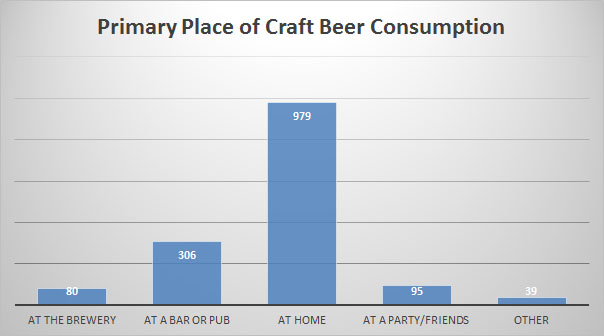

Craft beer is primarily consumed at home. 65% of all respondants said that their primary place of consumption is at home.

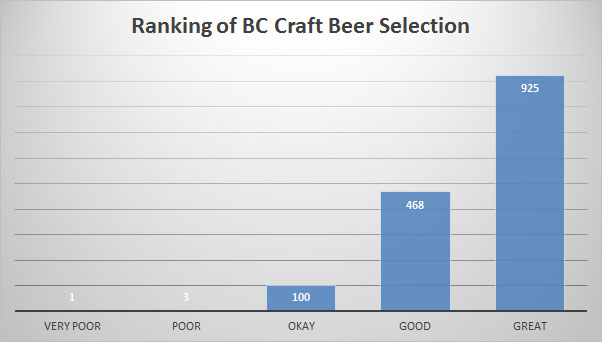

BC Craft Beer has better selection than ever before. 93.1% of all survey responses said that selection was good or great.

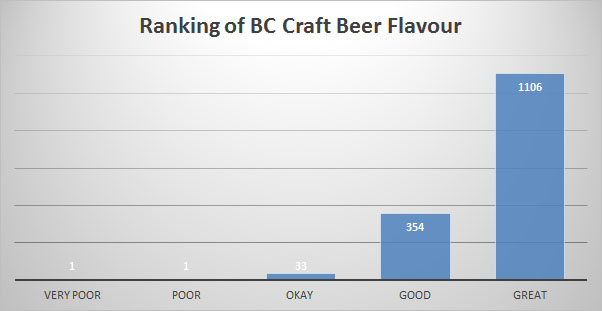

If you thought the selection was good, 99.0% of all survey respondents said that BC Craft Beer flavour was either good or great!

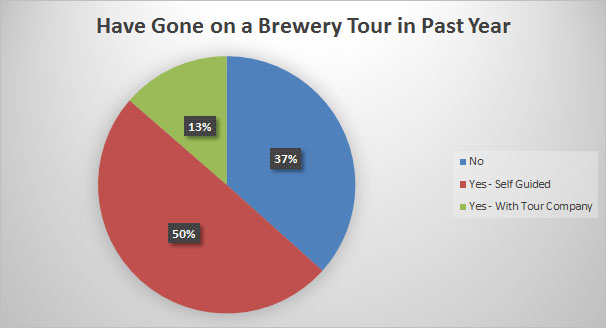

Brewery Tours are something that is easily done on your own or if you want the ultimate experience there are tour companies that will escort you to as many as four different breweries in a single afternoon. Of respondants 50% have conducted a self-guided tour while 13% have gone on a tour experience with a Brewery Tour company.

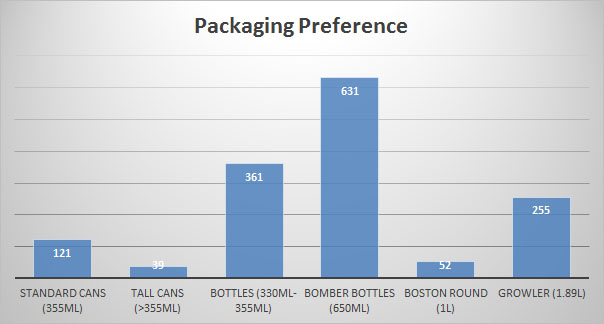

Last up is packaging preferences. This question segways into the 2nd article relating to the 2014 BC Craft Beer Survey. In part #2 we will compare key statistics with the 2013 results and show how preferences and opinions are changing over time. According to survey responses in 2014 43% of respondents prefer Bomber bottles, 25% standard bottles, 17% Growlers, 8% standard cans, 4% Boston rounds, and 3% tall cans.

If you were counting along the way you will have seen that our estimates put just over 1500 people have contributed $1.08 Million Dollars into the British Columbia Market.

See how things changed between 2013 and 2014 here

In making calculations where 10+ is a response option, the value of 10 was used in all circumstances.

[…] Part 1 – The State of Craft Beer […]

Great breakdown as always. This is a great article for the entire industry. New breweries can see that bombers are the way to go and established ones can look at change. I am surprised growler percentage isn’t higher. Maybe if Boston round, growlers and the new crowlers were combined it would be more representitive of what I expected.

The quality and styles of beer have really exploded this year and have really upped the anti. It’s a good time to be a beer nut!

Excellent information! How can I get a soft copy of this survey and the next part as well?

[…] See the results of the 2014 survey […]